UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

| | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

or

| TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number:

Aqua Metals, Inc.

(Exact name of registrant as specified in its charter)

| | |

| (State or Other Jurisdiction of | (I.R.S. Employer Identification |

(Address of principal executive offices)

(

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act

| Title of each class of stock: | Trading symbol | Name of each exchange on which registered: | ||||||

| | | The |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company (as defined in Rule 12b-2 of the Act):

| Large accelerated filer | ☐ |

| Accelerated filer | ☐ | |||||||||||||

|

|

|

| |||||||||||||||

| | ☒ |

| Smaller reporting company | | |||||||||||||

|

| Emerging Growth Company | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b) by the registered public accounting firm that prepared or issued its audit report.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

State the aggregate market value of voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter: $

The number of shares of the registrant’s common stock outstanding as of March 18, 2025 was

DOCUMENTS INCORPORATED BY REFERENCE

None.

CAUTIONARY NOTICE

This annual report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Those forward-looking statements include our expectations, beliefs, intentions and strategies regarding the future. Such forward-looking statements relate to, among other things,

| • |

our ability to have our Aqua Refining solutions gain market acceptance; | |

| • | our ability to acquire addition working capital on reasonable terms, as needed and on a timely basis. |

| • |

our intentions, expectations and beliefs regarding anticipated growth, market penetration and trends in our business; |

| • |

the timing and success of our plan of commercialization; |

| • |

our ability to demonstrate the operation of our AquaRefining process on a commercial scale; |

| • |

our ability to successfully apply our AquaRefining technology to the recycling of lithium-ion batteries; |

| • |

the effects of market conditions on our stock price and operating results; |

| • |

our ability to maintain our competitive technological advantages against competitors in our industry; |

| • |

our ability to maintain, protect and enhance our intellectual property; |

| • |

the effects of increased competition in our market and our ability to compete effectively; |

| • |

costs associated with defending intellectual property infringement and other claims; |

| • |

our expectations concerning our relationships with suppliers, partners and other third parties; and |

| • |

our ability to comply with evolving legal standards and regulations, particularly concerning requirements for being a public company and environmental regulations; |

These and other factors that may affect our financial results are discussed more fully in “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in this report. Market data used throughout this report is based on published third party reports or the good faith estimates of management, which estimates are presumably based upon their review of internal surveys, independent industry publications and other publicly available information. Although we believe that such sources are reliable, we do not guarantee the accuracy or completeness of this information, and we have not independently verified such information. We caution readers not to place undue reliance on any forward-looking statements. We do not undertake, and specifically disclaim any obligation, to update or revise such statements to reflect new circumstances or unanticipated events as they occur, and we urge readers to review and consider disclosures we make in this and other reports that discuss factors germane to our business. See in particular our reports on Forms 10-K, 10-Q, and 8-K subsequently filed from time to time with the Securities and Exchange Commission.

| Item 1. |

Background

We were formed as a Delaware corporation on June 20, 2014, for the purpose of engaging in the business of recycling metals through an innovative, proprietary and patent-pending process that we developed and named “AquaRefining.” In 2015, Aqua Metals developed a breakthrough metal recycling technology that utilizes a clean, closed-loop process that can produce high-purity metal. We believe this innovative approach can deliver raw materials back into the manufacturing supply chain while reducing emissions and toxic byproducts and creating a safer work environment. In particular, the modular AquaRefining systems have already demonstrated the ability to recover critical minerals from both lithium-ion and lead acid batteries and can reduce the cost and environmental impact of battery recycling.

Aqua Metals has a history of battery recycling, having first owned and operated a lead acid battery recycling facility between 2017 and 2019. This breakthrough technology was initially applied in the lead acid battery (LAB) recycling industry, building the first integrated recycling system for breaking LAB and recovering pure metal utilizing our innovative and patented smelterless AquaRefining technologies. In 2019, we operated our demonstration AquaRefinery at commercial quantity production levels and produced over 35,000 ‘AquaRefined’ ingots operating twenty-four hours a day, seven days a week for sustained periods of time.

In February 2021, we announced our entry into the lithium-ion battery (LiB) recycling market through a key provisional patent we filed that applies the same innovative AquaRefining approach. We believe our entry into lithium-ion battery recycling positions Aqua Metals to capitalize on the surging demand for critical minerals driven by the global energy transition, expected to create a $400 billion market by 2030. In August 2021, we announced we had established our Innovation Center in the Tahoe-Reno Industrial Center (TRIC) focused on applying our proven technology to LiB recycling research, development and prototyping.

During the first half of 2022, we announced our ability to recover copper, lithium, nickel, cobalt and manganese from lithium-ion battery ‘black mass’ at bench scale at the Company’s Innovation Center. During 2022, we built our fully-integrated pilot system, located within the Company’s Innovation Center, which is designed to enable Aqua Metals to be the first company in North America to recycle battery minerals from black mass, sell them in the U.S. and position the Company as the first sustainable LiB recycler in North America to align with the U.S. government’s goal of retaining strategic battery minerals within the domestic supply chain.

During 2022, we conducted environmental comparisons based on Argonne National Lab’s modeling of lithium battery supply chains – called EverBatt. The initial results indicate that AquaRefining is a cleaner and more sustainable approach to LiB recycling, producing far less CO2 waste streams than smelting or chemical-driven hydrometallurgical processes currently on the market. In December 2022, we completed equipment installation and began to operate our first-of-a-kind LiB recycling facility, utilizing renewable electricity as the reagent to recycle instead of intensive chemical processes, fossil fuels, or high-temperature furnaces. In January of 2023, Aqua Metals recovered its first metals from recycling lithium batteries using the patent-pending Li AquaRefining process.

In February 2023, we acquired a five-acre parcel of land with an existing building to begin development of our Li AquaRefining recycling campus at TRIC. When fully developed, the facility we envision is designed to process lithium-ion battery material using our proprietary Li AquaRefining technology. Subject to our receipt of the required additional capital, we expect to complete development of phase one, including all equipment installation within 3-4 quarters of securing the additional capital and to complete the commissioning and scaling of this operation at the new campus within 2 quarters of completion of the development. The Company is planning for a phased development of the campus, beginning with the already commenced redevelopment of an existing building on-site into the first commercial-scale Li AquaRefinery.

In the first half of 2024, we made significant progress on the construction of the planned first phase of the commercial Li AquaRefinery. We continue to pursue the required funding for the completion of the phase one development of our five‑acre recycling campus through various sources, including debt, project finance, joint venture and strategic investment options. At the end of 2024, we completed the first multi-week continuous 7 day x 24 hour operation campaign at our pilot facility, demonstrating the ability to deliver exceptional recovery rates and produce battery-grade critical minerals.

In February, 2025, the Company announced its expanded vision to more than double the output of lithium carbonate by deferring the plating of nickel and cobalt to metal form until the next phase. We believe this will allow for several potential improvements to the early years of scaling – reduced CAPEX by simplifying the product set to lithium carbonate and MHP (Mixed Hydroxide Precipitates), more volume of product due to the simplification, further de-risk with the simplified product set, more revenue and overall operating margins with a much improved payback on remaining capital to be financed. The Company continues to seek the funding to complete the phase 1 operation.

Effective November 5, 2024, we effected a one-for-20 reverse stock split of our issued and outstanding common shares. All share and share price information set forth in this report has been adjusted retrospectively to reflect this stock split.

Unless otherwise indicated, the terms “Aqua Metals,” “Company,” “we,” “us,” and “our” refer to Aqua Metals, Inc. and its wholly owned subsidiaries.

All references in this report to “ton” or “tonne” refer to a metric ton, which is equal to approximately 2,204.6 pounds.

Overview

Aqua Metals is seeking to reinvent metal recycling with its patented and patent-pending AquaRefining™ technologies. Aqua Metals is focused on developing cleaner and safer metals recycling through innovation. We believe Aqua Metals can expand the development of breakthrough technologies for sustainable metal recycling and deliver high-value critical minerals back into the manufacturing supply chain while reducing emissions and toxic byproducts and creating much safer work environments.

Aqua Metals has invested in breakthrough metals recycling methodologies that we believe are environmentally responsible, economically competitive, and will help retain critical strategic metals within the U.S. while enabling domestically produced, sustainably produced, recycled metals to enter the supply chain and lower sole reliance on unsafe and toxic mining operations. Since 2015, Aqua Metals has developed breakthrough metal recycling technologies that utilize a clean, closed-loop process that can produce ultra-high purity metals. AquaRefining is designed to deliver raw materials back into the manufacturing supply chain, and replaces the need for polluting furnaces and hazardous chemicals with electricity-powered electroplating to recover valuable metals and materials from spent batteries with higher purity, lower emissions, and minimal waste.

We believe Aqua Metals' regenerative electro-hydrometallurgical recycling method potentially offers a substantial improvement over traditional pyrometallurgical and hydrometallurgical recycling techniques, which produce much higher emissions, lower recovery rates, and significant landfill waste. We believe the AquaRefining process has the potential to vastly reduce the environmental impact of recycling lithium batteries as compared to other processes while providing a higher yield of high-purity metals essential for the burgeoning US battery manufacturing industry.

We are in the process of demonstrating that Li AquaRefining can create the highest quality and highest yields of recovered minerals from lithium-ion batteries, with lower waste streams and lower costs than alternatives. With the proven ability to recover valuable metals from lithium-ion batteries at our pilot facility in the TRIC, our goal is to demonstrate our ability to process commercial quantities of high-purity lithium hydroxide and/or carbonate, nickel, cobalt, manganese dioxide, and copper in pure forms that can be sold to the general metals and superalloy markets, and can be made into battery precursor compound materials with proven processes that are already used in the battery industry.

The Company is also exploring additional innovative applications of AquaRefining across metals recycling industries at our Innovation Center, including recycling emerging battery chemistries and opportunities to develop additional products for sale to customer specifications.

Our Markets

Aqua Metals’ AquaRefining process produces high purity metals and alloys that can be returned into the battery manufacturing supply chain or sold into metals markets for use across various advanced manufacturing industries. This combination of approaches and the broad applicability of the end products we aim to produce enables Aqua Metals to create low-emissions inputs for the battery supply chain or to help decarbonize other sectors that utilize these critical metals and superalloys – creating a more resilient and adaptable business model for the Company as a whole.

Metals Markets

Most of the minerals and metals that can be recovered in the recycling of batteries of various chemistries are also globally traded commodities. Lead, copper, cobalt, nickel, and other metals can be recovered and sold in pure metal form into these markets at the prevailing price or sold directly to a customer at a price set relative to the current market price.

For example, battery metals are globally traded metal commodities. Metals such as lead for LABs and nickel, cobalt, copper and lithium for LIBs are the essential components for the world’s rechargeable batteries. These metals are globally traded primarily on the London Metals Exchange (LME) and the Shanghai Metals Exchange (SHME) in China also trades these elements. In their pure forms, the other minerals that Aqua Metals intends to recover from spent batteries can be sold into these global markets. Unlike lead markets where recycled mineral content achieves up to 90% of new LAB batteries in a mature industry, lithium and related metals recycling currently achieves only 1-3% recycled mineral content of new LiB batteries, relying almost entirely on newly mined ore and refining to meet global demand.

As noted above, although metals are traded as a commodity on the various global exchanges, the major sales are directly between producers/traders and users (whom are typically battery manufacturers). The LME daily price is used as the benchmark in forming the basis of physical trades, forward contracts, and hedge strategies for both primary and secondary metals, in metal form. Based on market and product knowledge with buyers of metals in the U.S. and global metals markets, different grades (termed alloys) of metal are traded at a premium to the base LME price. Metal alloys, which are typically designed specifically for the customer, are also sold at a premium above the base LME, whereas byproducts (generally lower purity, compounds, or scrap) are traded at a discount to the LME as they are based on the underlying metals content and its form.

The Lithium Battery Market

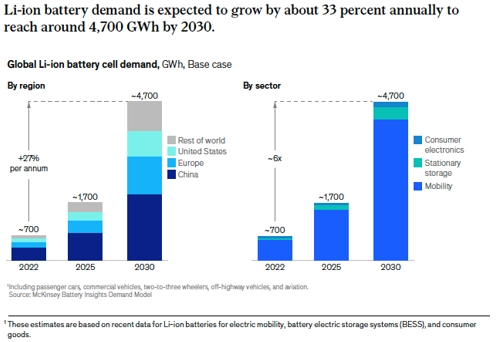

Global demand for Li-ion batteries is expected to soar over the next decade, with the number of GWh required increasing from about 700 GWh in 2022 to around 4.7 TWh by 2030 (Figure 1 below). Batteries for mobility applications, such as electric vehicles (EVs), will account for the vast bulk of demand in 2030—about 4,300 GWh; an unsurprising trend seeing that mobility is growing rapidly. This is largely driven by three major drivers:

| ● |

A regulatory shift toward sustainability, which includes new net-zero targets and guidelines, including Europe’s “Fit for 55” program, the US Inflation Reduction Act, the 2035 ban of internal combustion engine (ICE) vehicles in the EU and in the State of California in the U.S., and India’s Faster Adoption and Manufacture of Hybrid and Electric Vehicles Scheme. |

| ● |

Greater customer adoption rates and increased consumer demand for greener technologies (up to 90 percent of total passenger car sales will involve EVs in selected countries by 2030). |

| ● |

Announcements by 13 of the top 15 OEMs to discontinue production of ICE vehicles and achieve new emission-reduction targets. |

Figure 1: Growth of the Li-ion Battery Market Battery

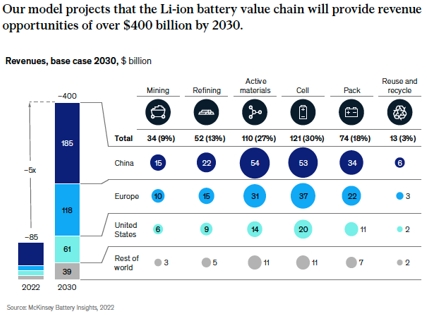

Battery energy storage systems (BESS) are expected to have a CAGR of 30 percent, and the GWh required to power these applications in 2030 will be comparable to the GWh needed for all applications today. China could account for 45 percent of total Li-ion demand in 2025 and 40 percent in 2030—most battery-chain segments are already mature in that country. Nevertheless, growth is expected to be highest globally in the EU and the United States, driven by recent regulatory changes, as well as a general trend toward localization of supply chains. In total, at least 120 to 150 new battery factories will need to be built between now and 2030 globally to have sufficient capacity to meet predicted demand. In line with the surging demand for Li-ion batteries across industries, it is projected that revenues along the entire value chain will increase 5-fold, from about $85 billion in 2022 to over $400 billion in 2030 (Figure 2). Active materials and cell manufacturing may have the largest revenue pools. Mining is not the only option for sourcing battery materials since recycling is also an option. Although the recycling segment is expected to be relatively small in 2030, it is projected to grow more than three-fold in the following decade, when more batteries reach their end-of-life and greater quantities of manufacturing scrap material become available for recycling.

Figure 2: Li-ion Revenue Opportunities through 2030

Lithium Batteries

EV batteries are powered by a battery pack made up of individual cells. Each cell has 4 components: the cathode, anode, separator, and electrolyte. Lithium-ion batteries use different raw materials for each of the components. The most common material used for the anode is graphite. The most widely used metal for the cathode is metal oxides that are combinations of lithium, cobalt, nickel, manganese, and aluminum. The electrolyte is generally made using acidic salts and solvents such as sulfuric acid and there are also solid-state silicon-based alternatives under development and early deployments have begun. The separator is usually created using a porous, polyolefin material like polyethylene or polypropylene.

Lithium-ion battery recycling is the method of taking EV batteries and splitting it into its components, ultimately into the original raw materials (lithium, nickel, cobalt, etc.) that can be reused in new batteries. While making lithium-ion batteries for EVs is important to address climate change, the batteries themselves are harmful to the environment if left in landfills or burned. Currently, only a small fraction of lithium-ion batteries are recycled and that must get close to 100% both to avoid environmental issues and to recapture the critical minerals in those spent batteries to feed the massive demand growth curve. Battery recycling helps address this problem, but current pyro-based battery recycling technology (smelting) also creates harmful emissions, potentially creating new climate problems faster than they are being solved. There are alternative hydro-based technologies available and rely on older methodologies that are known to create significant waste streams, potentially with more waste than product recovered, which have their own negative environmental and economic impacts.

Black Mass

Lithium-ion batteries are comprised of valuable metals such as lithium, copper, manganese, cobalt, and nickel. Once a battery is retired, the batteries can be collected, fully discharged, then shredded and base metals are separated to prepare them for recycling. This shiny, metallic mixture is what is called ‘black mass’—and it contains all the valuable metals that make up battery anodes and cathodes, the most expensive parts of a battery and the companies that collect and process batteries into black mass are referred to as ‘shredders’. The typical black color is due to the high concentrations of graphite contained in the anodes of batteries, which has a very dark black color. Black mass makes up about 40-50% of the total weight of an EV battery. Materials like the binder, copper, electrolytes, plastics, aluminum, and steel have been physically separated out by shredders before being recycled.

There are two main processes to producing black mass:

| 1. |

Pyrometallurgy: some black mass producers will use high temperatures to burn off unwanted materials like plastics and remaining electrolyte. This can create hazardous emissions and waste that must be captured or mitigated, and result in less recovered material. |

| 2. |

Hydrometallurgy: many producers use solution-based techniques—using water, chemicals and electricity to crush and separate the materials from a battery. This eliminates the need for polluting furnaces and energy intensive processing, creating a lower-carbon black mass. |

Aqua Metals specifically partners with producers that use non-pyro processes in order to create black mass to meet their own objectives for creating low-carbon recycled materials. The exact composition of black mass can vary considerably based on a number of factors. To start, there are many different types of lithium-ion batteries and manufacturing scrap forms, which will revert back to a mix of different elements and different ratios, including lithium, nickel, iron, titanium, copper, cobalt, manganese, and others (their use of lithium is the commonality).

Each manufacturer also has their own specific ‘recipe’ for their cathodes, cell type/form factors, as well as module type and pack assembly for different applications (cell phones, laptops, electric vehicles, etc.). Currently, the most popular types of lithium-ion batteries in the world incorporate significant amounts of nickel, cobalt, lithium, and manganese—so black mass produced today will typically have varying concentrations of each.

AquaRefining Process

We developed AquaRefining to be a cleaner and modular alternative to smelting and chemical-based recycling methods. Our process has two key elements, both of which are integral to our issued patents and pending-patent applications. The first is our use of proprietary, non-toxic solvents that dissolves metal compounds. The second is a proprietary electrochemical process and our modular Aqualyzer cells that selectively target each critical element and converts the dissolved metal compounds into high purity metals and/or salts.

The AquaRefining process begins with the processing of crushed used batteries either in the form of paste (for LAB) or, black mass (for LIB). The active materials are first processed to remove sulfur and then dissolved in our solvent. Metals are plated from the solvent using our patented and patent-pending process allowing the solvent to be reused.

We have demonstrated at bench scale and subsequently in our pilot facility that our lithium battery AquaRefining process can generate cobalt, lithium hydroxide or carbonate, copper, nickel, and manganese dioxide from lithium-ion battery black mass. A significant benefit of our AquaRefining process is that it can produce higher yields of higher purity, and thus higher value product than that derived from primary smelters with product from secondary sources.

Another significant benefit of our process is that we designed our AquaRefining equipment to be manufactured on a purpose-built production line in standard sized Aqualyzers. This is not possible with the smelting process, as smelters need to be constructed on site. This gives us the ability to provide AquaRefining systems with varying capacities to meet the specific needs of potential customers and suppliers. We have also developed an integrated software and portal called PureMetrics that keeps track of production and key operating metrics.

Recycling is subject to a variety of domestic and international regulations related to hazardous materials, emissions, employee safety and other matters. While our operations will be subject to these regulations, we believe that one of our potential advantages will be our ability to conduct battery recycling operations with less regulatory cost and burden than smelting operators due to the nature of our process. One of our key initiatives is and will continue to be, to educate regulators and the public as to the environmental benefits of AquaRefining. We believe that we have the potential to develop a business model that offers the opportunity to conduct, in an environmentally friendly manner, an important recycling activity that historically has been conducted in an often highly polluting manner.

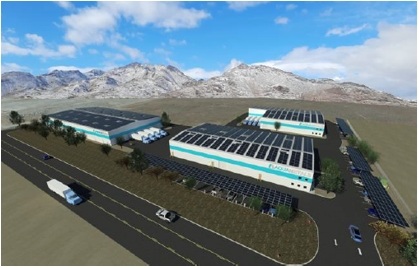

Project Site

Aqua Metals is in the process of building a new lithium-ion battery recycling facility to be located within Storey County, Nevada (the “Project”). The Project is located at 2955 & 2999 Waltham Way, McCarran, NV 89434 (the “Commercial Facility”). Aqua Metals operates a demonstration scale facility at 160 Denmark Drive, McCarran, NV 89434 (the “Innovation Center”) which utilizes the equivalent equipment and technology as is expected to be constructed and operated in the Project.

Figure 3: Aqua Metals Site Rendering

Highlights include:

| ● |

Five-acre campus designed to ultimately process 7,000 MT of lithium-ion battery black mass annually |

| ● |

Tahoe-Reno Industrial Center campus at the heart of Nevada’s lithium battery supply chain |

| ● |

Foreign Trade Zone designation |

| ● |

Rendering of existing building and additional land available for future expansion |

Our Business Model

Aqua Metals is engaged in the business of applying its commercialized clean, water-based recycling technology principles to develop the clean and cost-efficient recycling solutions for both lead and lithium-ion (“Li”) batteries. Our recycling process is a patented hydrometallurgical and electrochemical technology that is an innovative, proprietary and patented process we developed and named AquaRefining. AquaRefining is a low-emissions, closed-loop recycling technology that replaces polluting furnaces and hazardous chemicals with electricity-powered electroplating to recover valuable metals and materials from spent batteries with higher purity, lower emissions, and with minimal waste. The “Aqualyzers” cleanly generate ultra-pure metal one atom at a time, closing the sustainability loop for the rapidly growing energy storage economy.

We are applying our sustainable recycling technology principles with the goal of developing the cleanest and most cost-efficient recycling solution for lithium-ion batteries. We believe our process has the potential to produce higher quality products at a lower operating cost without the damaging effects of furnaces and greenhouse emissions. We expect to recover lithium hydroxide or lithium carbonate, copper, nickel, cobalt, and other compounds in a salable form to either be sold directly to lithium battery CAM manufactures or the commodities market. Aqua Metals estimates the total addressable market for lithium-ion battery recycling will grow to exceed lead battery recycling by the end of the decade. Unlike the mature lead recycling market, the deployed lithium-ion battery recycling infrastructure to serve market growth does not exist today.

Our business strategy focuses on developing and operating Li AquaRefining recycling facilities to meet the rising demand for critical metals used in lithium-ion batteries. This demand is driven by innovations in automobile batteries, the expansion of internet data centers, and alternative energy applications such as solar, wind, and grid-scale storage. Additionally, we aim to commercialize our AquaRefining process by licensing our technology to third parties and forming joint ventures and strategic partnerships with battery manufacturers and recyclers.

We are in the process of demonstrating that Li AquaRefining, which is fundamentally non-polluting, can create the highest quality and highest yields of recovered minerals from lithium-ion batteries with lower waste streams and lower costs than existing alternatives. Throughout 2023 and 2024, we have demonstrated at our pilot facility our ability to recover key valuable minerals in lithium-ion batteries, such as lithium hydroxide or lithium carbonate, copper, nickel, cobalt, and other compounds. Our goal is to process commercial quantities of nickel, cobalt, and copper in a pure metal form that can be sold to the general metals and superalloy markets and can be made into battery precursor compound materials with known processes already used in the mining industry. We have operated the first Li AquaRefining pilot plant in 2023 and in 2024. The location for the pilot demonstration facility is currently the Innovation Center with expansion to happen at our new 5-acre recycling campus to commercial quantities. Once fully completed, and based on our new expanded vision to more than double the output of lithium carbonate by deferring the plating of nickel and cobalt to metal form until the next phase, our first commercial facility is designed to process ~7,000 tonnes / year or more of battery materials, which would be enough material to build ~70,000 average EVs or ~300,000 average home energy storage systems. We are proceeding with a phased development approach, and commenced phase one of our campus.

Our focus for the lithium market includes operating our first-of-a-kind lithium battery recycling facility, utilizing electricity to recycle instead of intensive chemical processes, fossil fuels, or high-temperature furnaces. We are also exploring partnership and/or joint venture agreements, particularly as our Li AquaRefining matures. We believe that Aqua Metals is in a position to become one of the few critical minerals recovery players for which our environmental and economic value proposition should generate both great commercial wins and potentially government grants to accelerate our expansion and progress.

The market for lithium-ion batteries is global in scale but local in nature and execution, with large differences in local regulation, custom and practice, and access to transportation and electricity costs. In some regions, it is highly regulated, and in others it is not. Consequently, we are evolving our business model to commercialize our technology optimally across multiple locations.

Competition

Our development of recycling technology for lithium-ion batteries is a unique approach to extracting the high-value metals compared to the array of other potential solutions under development. Currently, smelting is the only commercially proven process for recycling lithium-ion batteries. The smelting process utilizes multiple high emissions steps with low yields to produce materials that typically require further refining before being utilized to manufacture new batteries. Over the next decade and beyond, when the volume of used batteries becomes significant, smelting will likely not be a viable solution due to the negative environmental impact and likelihood of regulatory restrictions on emissions. The other technologies currently under development utilize a predominately hydrometallurgical approach that consumes significant amounts of chemicals to extract the metals resulting in high cost and excessive waste streams. Our approach is a hybrid of hydrometallurgical and electrometallurgical processes like the process we have commercialized for lead, we call it “Li AquaRefining.” We believe that Li AquaRefining, as demonstrated through our lab-scale, bench-scale, and now pilot-scale operations, requires fewer chemicals, generates less waste, and produces higher-purity products at a lower cost compared to both smelting and standard hydrometallurgy.

The lithium-ion battery recycling market is significantly different from that of the lead recycling market in that it is a nascent industry. With no predominant technology to displace, our goal is to enable new and existing recyclers across the globe with Li AquaRefining as a best-in-class solution for meeting the supply chain demands of the lithium-ion battery industry as well as meeting the environmental needs of the planet and the corporations seeking to achieve net zero emissions.

The competitive advantages of the Aqua Metals project include:

| ● |

Replaces furnaces and heavy chemical use with 100% electricity-powered and closed-loop recycling, creating fundamentally non polluting, cost-efficient solution that generates minimal waste |

| ● |

AquaRefining recovers all valuable materials, including Lithium Hydroxide, Lithium Carbonate, and Manganese Dioxide, which are not recovered by competing methods |

| ● |

Recovers the high-value metals lost in smelting (like lithium and manganese), and produces high purity products |

| ● |

Only Li-ion recycling method with pathway to net-zero operations |

| ● |

Strong IP protection: 45 global patents; 42 patents pending for recycling various battery chemistries, including lithium ion and lead acid |

| ● |

Only electro-hydrometallurgy recycler in North America |

| ● |

Safer work environment, less hazardous materials, eliminates constant trainloads of chemicals |

| ● |

Massive and growing global addressable market |

| ● |

Greenfield opportunity for partnerships and strategic alliances |

Intellectual Property Rights

We regard the protection of our technologies and intellectual property rights as an important element of our business operations and crucial to our success. We endeavor to generate and protect our intellectual property assets through a series of patents, trademarks, internal and external policy and procedures and contractual provisions.

Patent Portfolio

Currently, we have secured 3 US patents, 38 international patents, and 4 allowances (international) for recycling various battery chemistries, including lithium ion and lead acid batteries. In addition to the US patents, we have international patents/allowances in the African Regional Intellectual Property Organization, African Intellectual Property Organization, Australia, Brazil, Canada, Chile, China, the Eurasian Patent Organization, European Union, Honduras, India, Indonesia, Japan, Malaysia, Mexico, Peru, South Korea, South Africa, Ukraine, and Vietnam. We also have 42 US and foreign patent applications pending with patent applications pending in 20 additional non-US jurisdictions, across five distinct patent applications relating to certain elements of the technology underlying our AquaRefining process and related apparatus and chemical formulations. The claims of the granted patents substantially address the same subject matter and are drawn to various aspects of processing lead or lithium materials using an aqua refining process. Differences in the claim number and scope are due to local rules and practice as well as the target metal.

We intend to continue to prepare and file domestic and foreign patent applications covering expanding aspects and applications of our technology, as circumstances warrant.

There can be no assurance that any patents will issue from any of our current or any future applications. Also, any patents that may issue may not survive a legal challenge to their scope, validity, or enforceability, or provide significant protection for us. Competitors may work around our patents, so they are not infringing. Our patent portfolio and our existing policy and procedures safeguarding our trade secrets nonetheless may face challenges so that our competitors can copy our AquaRefining process.

Trademark Portfolio

We have filed for trademark registration in the US and foreign countries for the following trademarks:

| • |

AQUA METALS (14 foreign countries) |

| • |

AQUAREFINING (10 foreign countries) |

| • |

AQMS (US only) |

| • | AQUAREFINERY (9 foreign countries) |

Trade Secrets and Contract Protection

We have developed our internal policy and procedures in safeguarding our trade secrets and proprietary information. Our procedures generally require our employees, consultants, and advisors to enter into confidentiality agreements. These agreements provide that all confidential information developed or made known to the individual during the course of the individual’s relationship with us is to be kept confidential and not disclosed to third parties except under specific circumstances. In the case of our employees, the agreements provide that all of the technology that is conceived by the individual during the course of employment is our exclusive property. The development of our technology and many of our processes are dependent upon the knowledge, experience, and skills of key scientific and technical personnel.

Government Regulation

Our operations and the operations of our licensees in the United States will be subject to the federal, state, and local environmental, health and safety laws applicable to the reclamation of LABs and lithium based batteries. While the reclamation process itself is generally not subject to federal permitting requirements, depending on how any particular operation is structured, our facilities and the facilities of our licensees may have to obtain environmental permits or approvals from federal, state or local regulators to operate, including permits or regulatory approvals related to air emissions, water discharges, waste management, and the storage of batteries on-site should that become necessary. We may face opposition from local residents or public interest groups to the installation and operation of our or our licensee's facilities. Failure to secure (or significant delays in securing) the necessary approvals could prevent us from pursuing some of our planned operations and adversely affect our business, financial results, and growth prospects.

In addition to permitting requirements, our operations and the operations of our licensees are subject to environmental health, safety and transportation laws and regulations that govern the management of and exposure to hazardous materials such as the lead, acids, and other metals involved in reclamation. These include hazard communication and other occupational safety requirements for employees, which may mandate industrial hygiene monitoring of employees for potential exposure to lead. Failure to comply with these requirements could subject our business to significant penalties (civil or criminal) and other sanctions that could adversely affect our business. Changes to these regulatory requirements in the future could also increase our costs, require changes in or cessation of certain activities, and adversely affect the business.

The nature of our operations and the operations of our licensees involves risks, including the potential for exposure to hazardous materials such as lead, that could result in personal injury and property damage claims from third parties, including employees and neighbors, which claims could result in significant costs or other environmental liability. Our operations and the operations of our licensees also pose a risk of releases of hazardous substances, such as lead, acids, and other metals related to lithium batteries into the environment, which can result in liabilities for the removal or remediation of such hazardous substances from the properties at which they have been released, liabilities which can be imposed regardless of fault, and our business could be held liable for the entire cost of cleanup even if we were only partially responsible. Like any manufacturer, we and our licensees are also subject to the possibility that we may receive notices of potential liability in connection with materials that were sent to third-party recycling, treatment, and/or disposal facilities under the Federal Comprehensive Environmental Response, Compensation and Liability Act of 1980, as amended (“CERCLA”), and comparable state statutes, which impose liability for investigation and remediation of contamination without regard to fault or the legality of the conduct that contributed to the contamination, and for damages to natural resources. Liability under CERCLA is retroactive, and, under certain circumstances, liability for the entire cost of a cleanup can be imposed on any responsible party.

As our business expands outside of the United States, our licensed operations will be subject to the environmental, health and safety laws of the countries where we do business, including permitting and compliance requirements that address the similar risks as do the laws in the United States, as well as international legal requirements such as those applicable to the transportation of hazardous materials. Depending on the country or region, these laws could be as stringent as those in the US, or they could be less stringent or not as strictly enforced. In some countries in which we are interested in expanding our business, such as South America, Taiwan and China, the relevant environmental regulatory and enforcement frameworks are in flux and subject to change. Therefore, while compliance with these requirements will cause our business to incur costs, and failure to comply with these requirements could adversely affect our business, it is difficult to evaluate such potential costs or adverse impacts until such time as we decide to initiate operations in particular countries outside the United States.

Employees

As of the date of this report, we employ 11 people on a full-time basis. None of our employees are represented by a labor union.

Financial and Segment Information

We operate our business as a single segment, as defined by generally accepted accounting principles. Our financial information is included in the consolidated financial statements and the related notes.

Available Information

Our website is located at www.aquametals.com and our investor relations website is located at https://ir.aquametals.com/. Copies of our Annual Report on Form 10-K, Quarterly Report on Form 10-Q, Current Reports on Form 8-K, and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, are available, free of charge, on our investor relations website as soon as reasonably practicable after we file such material electronically with or furnish it to the Securities and Exchange Commission, or the SEC. The SEC also maintains a website that contains our SEC filings. The address of the site is www.sec.gov. The contents of our website are not intended to be incorporated by reference into this Annual Report on Form 10-K or in any other report or document we file with the SEC, and any references to our websites are intended to be inactive textual references only.

| Item 1A. |

Investing in our common stock involves a high degree of risk. Before purchasing our common stock, you should read and consider carefully the following risk factors as well as all other information contained in this report, including our consolidated financial statements and the related notes. Each of these risk factors, either alone or taken together, could adversely affect our business, operating results and financial condition, as well as adversely affect the value of an investment in our common stock. There may be additional risks that we do not presently know of or that we currently believe are immaterial, which could also impair our business and financial position. If any of the events described below were to occur, our financial condition, our ability to access capital resources, our results of operations and/or our future growth prospects could be materially and adversely affected and the market price of our common stock could decline. As a result, you could lose some or all of any investment you may make in our common stock.

Risks Relating to Our Business and Operations

We have a limited operating history and limited revenue producing operations and are currently focusing on developing our lithium battery recycling. Therefore, it is difficult for potential investors to evaluate our business. We formed our corporation in June 2014. From inception through December 31, 2024, we generated a total of $11.7 million of revenue, all of which was derived primarily from the sale of lead compounds and plastics and, to a lesser extent, the sale of lead bullion and AquaRefined lead, and all but approximately $310,000 of which was derived prior to January 1, 2020 at our former LAB recycling facility. In the last three years, the business has been focused on completing the research and development of the application of our AquaRefining technology to the recycling of lithium-ion batteries and operating a lithium-ion recycling pilot plant. Based upon our success to date in recovering high value metals from lithium-ion batteries using our AquaRefining technology, we have commenced the development of a five-acre recycling campus designed to process up to 7,000 tonnes of lithium-ion battery material annually from our first phase. While we intend to continue to pursue our licensing business model, the development of our lithium-ion battery recycling facility represents a significant focus in our business strategy and course of operations. As of the date of this report, we estimate that we will begin to realize revenues from lithium-ion battery recycling with in three to four quarters after receiving funding, however we are unable to estimate when we expect to commence any meaningful commercial or revenue producing operations from either our licensing model or our lithium-ion battery recycling facility. Our limited operating history makes it difficult for potential investors to evaluate our technology or prospective operations and we are, for all practical purposes, an early-stage company subject to all the risks inherent in the initial organization, financing, expenditures, complications, and delays in a new business, including, without limitation:

| • |

our ability to successfully apply, and realize the expected benefits of applying, our AquaRefining technology to the plating of high value metals found in lithium-ion batteries, including cobalt, and nickel; |

| • |

the timing and success of our plan of commercialization and the fact that we have not entered into a commercial license for our AquaRefining technology and only have recently commenced the build out of our lithium-ion recycling facility; |

| • |

our ability to successfully develop our proposed lithium-ion recycling facility; |

| • |

our ability to demonstrate that our AquaRefining technology can recycle either LABs or lithium-ion batteries on a commercial scale; and | |

| • | our ability to license our AquaRefining process and sell our AquaRefining equipment to recyclers of LABs and lithium-ion batteries. |

Investors should evaluate an investment in us in light of the uncertainties encountered by developing companies in a competitive environment. There can be no assurance that our efforts will be successful or that we will ultimately be able to attain profitability.

We will need additional financing to execute our business plan and fund operations, which additional financing may not be available on reasonable terms or at all. As of December 31, 2024, we had total cash of $4.0 million and working capital of $(3.9) million. As of the date of this report, we believe that we will require additional capital in order to fund our current level of ongoing costs and our proposed business plan over the next 12 months as we move forward with our business strategy. We intend to acquire the necessary capital though debt financing or through the sale of equity. Funding that includes the sale of our equity may be dilutive. If such funding is not available on satisfactory terms, we may be unable to further pursue our business plan and we may be unable to continue operations, in which case you may lose your entire investment.

The report of our independent registered public accounting firm for the year ended December 31, 2024 states that there is substantial doubt about our ability to continue as a going concern within one year after the date that the financial statements are issued.

As of the date of this report, we have in excess of $4.0 million of secured indebtedness, the majority of which is held by related parties and all of which becomes due within the next nine months. In February 2023, we entered into a $3 million secured debt facility with Summit Investment Services, LLC, an entity controlled by Eric Gangloff, who subsequently became a member of our board of directors, and in December 2024 we conducted the private placement of $1.5 million of secured promissory notes with eight accredited investors, including certain of our executive officers and directors who purchased an aggregate of $1,200,000 of the private placement notes. The indebtedness under the Summit debt facility and the private placement notes are secured by all of our assets, with a few exceptions. All principal and interest under the Summit debt facility is due and payable on April 27, 2025 and all principal and interest under the private placement notes are due and payable on December 31, 2025. If we are unable to repay or refinance the secured debt in a timely manner, the debt holders can exercise their rights under their security agreements collateralizing their debt and foreclose on our assets. The fact that a majority of the debt is held by our officers and directors raises issues concerning potential conflicts of interest. There can be no assurance that we will be able to repay or refinance the secured debt in a timely manner.

We recently commenced the development of a lithium-ion recycling facility, however we are in the early stages of developing the facility and there can be no assurance that we will be able to successfully develop the facility or, if we do, realize the expected benefits of the facility. In January 2023, we announced our plans to conduct the phased development of a five-acre recycling campus in the Tahoe-Reno Industrial Center, or TRIC, in McCarran, Nevada. The first phase of the facility is designed, when fully developed, to process up to 7,000 tonnes of lithium-ion battery material each year using our proprietary AquaRefining technology. On February 1, 2023, we closed on the acquisition financing and purchased the five-acre site, plus the existing 21,000 square foot building, and as noted elsewhere, in third quarter of 2023 we raised a net of $22.9 million from the sale of our common stock. In the second quarter of 2024 we raised a net of $7.3 million from the sale of our common stock. In the first half of 2024 we began the Phase One build-out of the facility. However, we will need additional financing to complete the build-out of Phase One, which we intend to pursue through conventional non-dilutive loans, potential government backed debt offerings, government grants or through the sale of our common stock via our current at-the-market offering. The Company is planning for a phased development of the campus, beginning with the already commenced redevelopment of an existing building on-site into the first commercial-scale Li AquaRefinery. Subject to our receipt of development financing on a timely basis, we expect to complete development of Phase One, including all equipment installation, within three quarters of receiving funding and to commence operations shortly thereafter. However, there can be no assurance we will be able to do so.

Our business is dependent upon our successful implementation of innovative technologies and processes and there can be no assurance that we will be able to implement such technologies and processes in a manner that supports the successful commercial roll-out of our business model. While much of the technology and processes involved in battery recycling operations are widely used and proven, our AquaRefining process is largely innovative and, to date, has been demonstrated on a modest scale of operations. While we have shown that our proprietary technology can produce AquaRefined metals from batteries on a small scale, we have not processed recycled batteries on a commercial scale. We recently commenced the development of a five-acre recycling campus designed to process lithium-ion batteries, however there can be no assurance that we will be able to complete the development of the recycling facility or, if we are able to do so, that we will be able to successfully process lithium-ion batteries on a commercial scale.

Our business model is new and has not been proven by us or anyone else. We are engaged in the business of producing recycled metals from LABs and high value metals from lithium-ion batteries through an innovative, and proven on a modest scale, technology. While the production of recycled batteries is an established business, to date virtually all recycled metals have been produced by way of traditional smelting processes. To our knowledge, no one has successfully produced recycled batteries in commercial quantities other than by way of smelting. In addition, neither we nor anyone else has ever successfully built a production line that commercially recycles batteries without smelting. Further, there can be no assurance that either we will be able to produce AquaRefined metals from batteries in commercial quantities at a cost of production that will provide us with an adequate profit margin. The uniqueness of our AquaRefining process presents potential risks associated with the development of a business model that is untried and unproven.

We have performed the research and development of the application of our AquaRefining technology to the recycling and recovery of lithium-ion batteries, however there can be no assurance that our efforts will be successful. In September 2021, we announced the establishment of our Innovation Center, in McCarran, Nevada, focused on applying our AquaRefining technology to lithium-ion battery recycling research and development and prototype system activities. In 2021, we filed a provisional patent for recovering high-value metals from recycled lithium-ion batteries to complement the patents for AquaRefining. At the end of 2022 and throughout 2023 and 2024, we successfully recovered all valuable materials from spent lithium batteries at production scale using our AquaRefining technology: lithium hydroxide, copper, nickel, cobalt, and manganese dioxide. We also operated our pilot plant throughout 2024. We are continuing our efforts to improve our Li AquaRefining process; however, there can be no assurance that our efforts will be successful or that we will be able to conduct the recycling and recovery of the high value metals from lithium-ion batteries on a commercial scale.

Our business strategy includes licensing arrangements and entering into joint ventures and strategic alliances, however as of the date of this report we have no such agreements in place and there can be no assurance we will be able to do so. Failure to successfully integrate such licensing arrangements, joint ventures, or strategic alliances into our operations could adversely affect our business. We propose, as one of our business strategies, to commercially exploit our AquaRefining process by licensing our technology to third parties and entering into joint ventures and strategic relationships with parties involved in the manufacture and recycling of batteries. We are also currently seeking to negotiate agreements with others. However, there can be no assurance we will be able to conclude a licensing agreement with any partners, or that we will be able to do so on terms that benefit us. Our ability to enter into licensing, joint ventures and strategic relationships with third parties will depend on our ability to demonstrate the technological and commercial advantages of our AquaRefining process, of which there can be no assurance. Also, even if we are able to enter into licensing, joint venture or strategic alliance agreements, there can be no assurance that we will be able to obtain the expected benefits of any such arrangements. In addition, licensing programs, joint ventures and strategic alliances may involve significant other risks and uncertainties, insufficient revenue generation to offset liabilities assumed and expenses associated with the transaction, potential additional challenges in protecting our intellectual property, and unidentified issues not discovered in our due diligence process, such as product quality, technology issues and legal contingencies. In addition, we may be unable to effectively integrate any such programs and ventures into our operations. Our operating results could be adversely affected by any problems arising during or from any licenses, joint ventures or strategic alliances.

Even if our licensees are successful in recycling batteries using our processes, there can be no assurance that the AquaRefined recycled metals will meet the certification and purity requirements of the potential customers. A key component of our business plan is the production of recycled metals through our AquaRefining process. Our customers will require that our AquaRefined metals meet certain minimum purity standards and, in all likelihood, require independent assays to confirm the metal’s purity. As of the date of this report, we have produced limited quantities of AquaRefined metals. We have not produced AquaRefined metals in significant commercial quantities and there can be no assurance that we will be able to do so or, that such metals will meet the required purity standards of our customers. Further, while we have recently commenced the application of our AquaRefining process towards the recovery of high value metals found in lithium-ion batteries, such as cobalt, nickel, lithium hydroxide, lithium carbonate, copper, and manganese dioxide, we have only recently begun the development of recycling of lithium-ion batteries, and there can be no assurance that our efforts will be successful or that we will be able to conduct the recycling and recovery of the high value metals from lithium-ion batteries on a commercial scale.

While we have been successful in producing AquaRefined metals in small volumes, there can be no assurance that either we or our licensees will be able to replicate the process, along with all of the expected economic advantages, on a large commercial scale either for us or our prospective licensees. While we believe that our development, testing and limited production to date of AquaRefined metals has validated the concept of our AquaRefining process, the limited nature of our operations to date are not sufficient to confirm the economic returns on our production of recycled metals. Further, we have only recently commenced commercial operations in the area of recycling of lithium-ion batteries. There can be no assurance that either us or our licensees will be able to produce AquaRefined metals from batteries in commercial quantities at a cost of production that will provide us and our proposed licensees with an adequate profit margin.

Our intellectual property rights may not be adequate to protect our business. As of the date of this report, we have 3 issued US patents, 38 international patents, and 4 international allowances related to our AquaRefining process.

We also have further patent applications pending in the United States and numerous corresponding patent applications pending in 20 additional jurisdictions relating to certain elements of the technology underlying our AquaRefining process and related apparatus and chemical formulations. However, no assurances can be given that any patent issued, or any patents issued on our current and any future patent applications, will be sufficiently broad to adequately protect our technology. In addition, we cannot assure you that any patents issued now or in the future will not be challenged, invalidated, or circumvented.

Even patents issued to us may not stop a competitor from illegally using our patented processes and materials. In such event, we would incur substantial costs and expenses, including lost time of management in addressing and litigating, if necessary, such matters. Additionally, we rely upon a combination of trade secret laws and nondisclosure agreements with third parties and employees having access to confidential information or receiving unpatented proprietary know-how, trade secrets and technology and employees sign severance agreements upon termination due to a reduction in force to protect our proprietary rights and technology. These laws and agreements provide only limited protection. We can give no assurance that these measures will adequately protect us from misappropriation of proprietary information.

Our processes may infringe on the intellectual property rights of others, which could lead to costly disputes or disruptions. The applied science industry is characterized by frequent allegations of intellectual property infringement. Though we do not expect to be subject to any of these allegations, any allegation of infringement could be time consuming and expensive to defend or resolve, result in substantial diversion of management resources, cause suspension of operations or force us to enter into royalty, license, or other agreements rather than dispute the merits of such allegation. If patent holders or other holders of intellectual property initiate legal proceedings, we may be forced into protracted and costly litigation. We may not be successful in defending such litigation and may not be able to procure any required royalty or license agreements on acceptable terms or at all.

Our internal computer systems, or those of our collaborators or other contractors or consultants, may fail or suffer security breaches, which could result in a material disruption of our product development programs. Our internal computer systems and those of our current and any future customers, vendors, licensees, collaborators and other contractors or consultants are vulnerable to damage from computer viruses, unauthorized access, natural disasters, terrorism, war and telecommunication and electrical failures. While we have not experienced any such material system failure, accident or security breach to date, if such an event were to occur and cause interruptions in our operations, it could result in a disruption of our research and development and our business operations, whether due to a loss of our trade secrets or other proprietary information or other similar disruptions. To the extent that any disruption or security breach were to result in a loss of, or damage to, our data or applications, or inappropriate disclosure of confidential or proprietary information, we could incur liability, our competitive position could be harmed and the further development and commercialization of our recycling technologies could be delayed.

We could be subject to risks caused by misappropriation, misuse, leakage, falsification or intentional or accidental release or loss of information maintained in the information systems and networks of our company and our customers, vendors, licensees, collaborators and other contractors or consultants, including personal information of our employees and others, and company and third-party confidential data. In addition, outside parties may attempt to penetrate our systems or those of our customers, vendors, licensees, collaborators and other contractors or consultants or fraudulently induce our personnel or the personnel of third parties to disclose sensitive information in order to gain access to our data and/or systems. We may experience threats to our data and systems, including malicious codes and viruses, phishing and other cyberattack. The number and complexity of these threats continue to increase over time. If a material breach of, or accidental or intentional loss of data from, our information technology systems or those of our customers, vendors, licensees, collaborators and other contractors or consultants occurs, the market perception of the effectiveness of our security measures could be harmed and our reputation and credibility could be damaged. We could be required to expend significant amounts of money and other resources to repair or replace information systems or networks. In addition, we could be subject to regulatory actions and/or claims made by individuals and groups in private litigation involving privacy issues related to data collection and use practices and other data privacy laws and regulations, including claims for misuse or inappropriate disclosure of data, as well as unfair or deceptive practices.

Although we develop and maintain systems and controls designed to prevent these events from occurring, and we have a process to identify and mitigate threats, the development and maintenance of these systems, controls and processes is costly and requires ongoing monitoring and updating as technologies change and efforts to overcome security measures become increasingly sophisticated. Moreover, despite our efforts, the possibility of these events occurring cannot be eliminated entirely. As we outsource more of our information systems to vendors, engage in more electronic transactions with third parties, and rely more on cloud-based information systems, the related security risks will increase and we will need to expend additional resources to protect our technology and information systems. In addition, there can be no assurance that our internal information technology systems or those of our customers, vendors, licensees, collaborators and other contractors or consultants will be sufficient to protect us against breakdowns, service disruption, data deterioration or loss in the event of a system malfunction, or prevent data from being stolen or corrupted in the event of a cyberattack, security breach, industrial espionage attacks or insider threat attacks which could result in financial, legal, business or reputational harm.

Risks Relating to Geopolitical, Macroeconomic and Industry Factors

Unfavorable geopolitical and macroeconomic developments could adversely affect our business, financial condition or results of operations. Our business could be adversely affected by conditions in the U.S. and global economies. Global economic uncertainty, inflation, changes in interest rates, supply chain disruptions, and fluctuations in foreign exchange rates can adversely affect our operations, profitability, and demand for our products and services.

Additionally, geopolitical tensions, trade restrictions, tariffs, and regulatory changes in key markets where we operate could impact our ability to source materials, manufacture products, or expand into new markets. Armed conflicts, economic sanctions, and political instability in various regions may disrupt our supply chains, increase costs, and limit growth opportunities. Furthermore, shifts in industry trends, technological advancements, and competitive pressures could require us to adapt our business model or invest significant resources to remain competitive. If we are unable to effectively manage these external risks, our financial performance and strategic objectives could be materially affected.

Any of the foregoing could harm our business. Any resulting financial impact cannot be reasonably estimated at this time but may materially affect our business and financial condition. The extent to which the foregoing impacts our results will depend on future developments, which are highly uncertain and cannot be predicted.

Our business may be negatively affected by labor issues and higher labor costs. Our ability to maintain our workforce depends on our ability to attract and retain new and existing employees. As of the date of this report, none of our employees are covered by collective bargaining agreements and we consider our labor relations to be acceptable. However, we could experience workforce dissatisfaction which could trigger bargaining issues, employment discrimination liability issues as well as wage and benefit consequences, especially during critical operation periods. We could also experience a work stoppage or other disputes which could disrupt our operations and could harm our operating results. In addition, legislation or changes in regulations could result in labor shortages and higher labor costs. There can be no assurance that we may not experience labor issues that negatively impact our operations or results of operations.

Global economic conditions could negatively affect our prospects for growth and operating results. Our prospects for growth and operating results will be directly affected by the general global economic conditions of the industries in which our suppliers, partners and customer groups operate. We believe that the market price of battery metal is relatively volatile and reacts to general global economic conditions. Our business will be highly dependent on the economic and market conditions in each of the geographic areas in which we operate. These conditions affect our business by reducing the demand for recyclable batteries and decreasing the price of battery metals in times of economic downturn and increasing the price of used batteries in times of increasing demand of recyclable batteries. There can be no assurance that global economic conditions will not negatively impact our liquidity, growth prospects and results of operations.

We are subject to the risks of conducting business outside the United States. A part of our strategy involves our pursuit of growth opportunities in certain international market locations. We intend to pursue licensing or joint venture arrangements with local partners who will be primarily responsible for the day-to-day operations. Any expansion outside of the U.S. will require significant management attention and financial resources to successfully develop and operate any such facilities, including the sales, supply and support channels, and we cannot assure you that we will be successful or that our expenditures in this effort will not exceed the amount of any resulting revenues. Our international operations expose us to risks and challenges that we would otherwise not face if we conducted our business only in the United States, such as:

| • |

increased cost of enforcing our intellectual property rights; |

| • |

diminished ability to protect our intellectual property rights; |

| • |

heightened price sensitivities from customers in emerging markets; |

| • |

our ability to establish or contract for local manufacturing, support and service functions; |

| • |

localization of our battery metals and components, including translation into foreign languages and the associated expenses; |

| • |

compliance with multiple, conflicting and changing governmental laws and regulations; |

| • |

compliance with the Federal Corrupt Practices Act and other anti-corruption laws; |

| • |

foreign currency fluctuations; |

| • |

laws favoring local competitors; |

| • |

weaker legal protections of contract terms, enforcement on collection of receivables and intellectual property rights and mechanisms for enforcing those rights; |

| • |

market disruptions created by public health crises in regions outside the United States; |

| • |

difficulties in staffing and managing foreign operations, including challenges presented by relationships with workers’ councils and labor unions; |

| • |

issues related to differences in cultures and practices; and |

| • |

changing regional economic, political and regulatory conditions. |

Risks Relating to Government Law and Environmental Regulations

U.S. government regulation and environmental, health and safety concerns may adversely affect our business. Our operations and the operations of our licensees in the United States will be subject to the federal, state and local environmental, health and safety laws applicable to the reclamation of batteries including the Occupational Safety and Health Act ("OSHA") of 1970 and comparable state statutes. Our facilities and the facilities of our licensees will have to obtain environmental permits or approvals to expand, including those associated with air emissions, water discharges, and waste management and storage. We and our licensees may face opposition from local residents or public interest groups to the installation and operation of our respective facilities. In addition to permitting requirements, our operations and the operations of our licensees are subject to environmental health, safety and transportation laws and regulations that govern the management of and exposure to hazardous materials such as the acids involved in battery reclamation. These include hazard communication and other occupational safety requirements for employees, which may mandate industrial hygiene monitoring of employees for potential exposure.

We and our licensees are also subject to inspection from time to time by various federal, state and local environmental, health and safety regulatory agencies and, as a result of these inspections, we and our licensees may be cited for certain items of non-compliance. Failure to comply with the requirements of federal, state and local environmental, health and safety laws could subject our business and the businesses of our licensees to significant penalties (civil or criminal) and other sanctions that could adversely affect our business. In addition, in the event we are unable to operate and expand our AquaRefining process and operations as safe and environmentally responsible, we and our licensees may face opposition from local governments, residents or public interest groups to the installation and operation of our facilities.

The development of new AquaRefining technology by us or our partners or licensees, and the dissemination of our AquaRefining process will depend on our ability to acquire necessary permits and approvals, of which there can be no assurance. As noted above, our AquaRefining processes will have to obtain environmental permits or approvals to operate, including those associated with air emissions, water discharges, and waste management and storage. In addition, we expect that any use of AquaRefining operations at our partner's facilities will require additional permitting and approvals. Failure to secure (or significant delays in securing) the necessary permits and approvals could prevent us and our partners and licensees from pursuing additional AquaRefining expansion, and otherwise adversely affect our business, financial results and growth prospects. Further, the loss of any necessary permit or approval could result in the closure of an AquaRefining facility and the loss of our investment associated with such facility.